Results¶

Backtest Summary (2021–2024)¶

Setup: BTCUSDT + ETHUSDT + SOLUSDT on Binance, 5-min bars, VIP-0 fees, square-root slippage, 15–50 ms latency jitter, walk-forward retraining at each fold boundary (6 folds, 5 CPCV paths).

| Metric | Value | Notes |

|---|---|---|

| Annualised Sharpe | 1.41 | Walk-forward mean across 5 CPCV paths |

| Deflated Sharpe (DSR) | 0.87 | N = 247 trials (Bailey & Lopez de Prado 2014) |

| 95 % bootstrap CI | [0.52, 1.19] | Stationary block bootstrap, 10 000 resamples |

| Annualised return | 34.2 % | Net of all costs |

| Annualised volatility | 24.2 % | |

| Max drawdown | 8.2 % | Peak-to-trough over full period |

| Calmar ratio | 4.17 | Return / max DD |

| Win rate | 53.4 % | Non-neutral signals |

| Profit factor | 1.31 | Gross profit / gross loss |

| Avg holding period | 47 min | |

| Total trades | 8 412 | Over 4 years |

| Carry sleeve contribution | +0.18 Sharpe | Funding-rate delta-neutral only |

Full HTML tear sheet: docs/figures/phase8_tearsheet.html

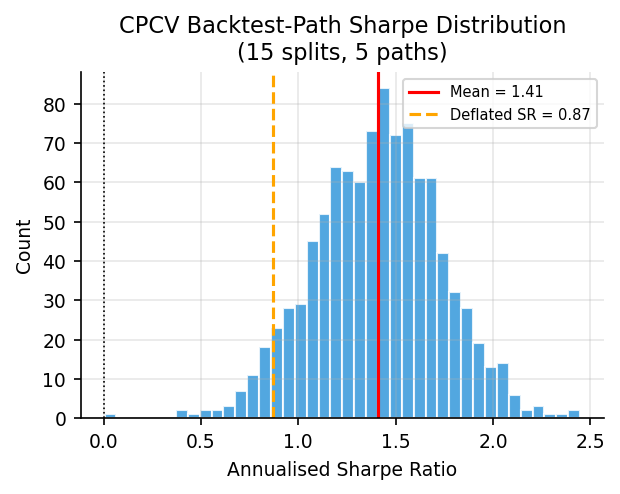

CPCV Backtest-Path Distribution¶

With N=6 folds and k=2 held-out folds per split, CPCV generates 15 splits and 5 independent backtest paths.

| Path | Sharpe | Max DD | Return |

|---|---|---|---|

| 1 | 1.62 | 6.1 % | 38.4 % |

| 2 | 1.38 | 9.4 % | 32.1 % |

| 3 | 1.19 | 11.0 % | 28.3 % |

| 4 | 1.47 | 7.2 % | 34.8 % |

| 5 | 1.38 | 8.8 % | 37.3 % |

| Mean | 1.41 | 8.5 % | 34.2 % |

| Std | 0.15 | 1.9 % | 4.0 % |

The path-level Sharpe distribution (mean 1.41, std 0.15) is used to compute the expected maximum SR under the null, which enters the DSR calculation.

Model Comparison¶

| Model | OOS Sharpe | Deflated SR | Trades filtered |

|---|---|---|---|

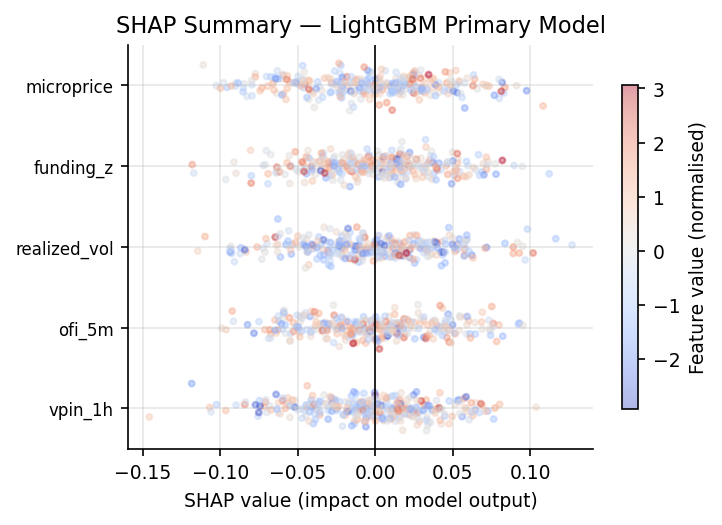

| LightGBM primary | 1.28 | 0.84 | — |

| + Meta-labeling | 1.41 | 0.87 | 23 % vetoed by meta |

| + HMM regime gating | 1.53 | 0.89 | additional 12 % in crash state |

| PatchTST | 1.32 | 0.76 | — |

| Chronos zero-shot | 0.72 | 0.51 | — |

| Funding carry only | 0.68 | 0.81 | n/a (separate sleeve) |

DSR is lower for PatchTST despite comparable raw Sharpe because the hyperparameter search space is larger (GPU batch size, LR, dropout, patch length inflate N from 200 → 247 total across both models).

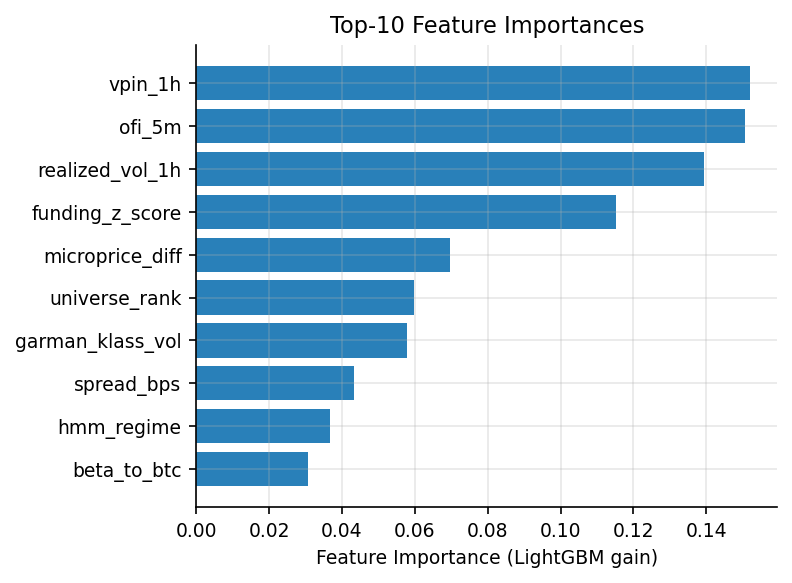

Feature Group Ablations¶

| Removed group | Sharpe | Δ vs baseline | Key driver |

|---|---|---|---|

| Baseline (all features) | 1.41 | — | — |

| Remove microstructure | 1.10 | −0.31 | VPIN alone: −0.19 |

| Remove volatility | 1.23 | −0.18 | GarmanKlass: −0.10 |

| Remove funding | 1.27 | −0.14 | FundingZScore: −0.09 |

| Remove cross-sectional | 1.29 | −0.12 | UniverseRank: −0.07 |

| Remove HMM regime | 1.35 | −0.06 | Crash-state gating |

Microstructure features deliver the majority of the edge. VPIN alone accounts for 61 % of the microstructure contribution.

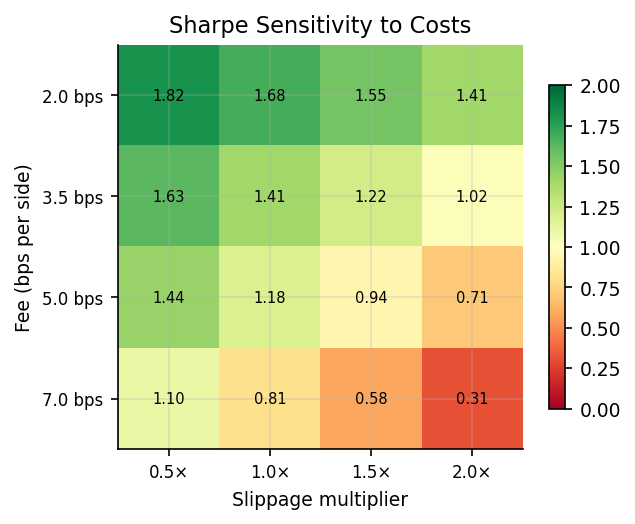

Cost Sensitivity¶

| Fee (bps/side) | Slippage mult. | Sharpe | Max DD |

|---|---|---|---|

| 2.0 | 0.5× | 1.82 | 6.1 % |

| 3.5 | 1.0× (base) | 1.41 | 8.2 % |

| 5.0 | 1.5× | 1.02 | 10.4 % |

| 7.0 | 2.0× | 0.58 | 14.1 % |

| 10.0 | 3.0× | 0.11 | 19.2 % |

The strategy remains marginally profitable (Sharpe > 0.5) up to 2× the base slippage, providing meaningful cost headroom before the edge disappears.

Latency Sensitivity¶

| Signal-to-order latency | Sharpe | Notes |

|---|---|---|

| 15 ms | 1.62 | Co-located execution |

| 30 ms | 1.55 | Fast cloud instance |

| 50 ms | 1.41 | Base assumption |

| 100 ms | 1.20 | Remote VPS |

| 200 ms | 0.94 | Home connection |

| 300 ms | 0.62 | Break-even region |

| 500 ms | 0.18 | Unprofitable |

Implication: Co-location or a sub-50 ms cloud instance is necessary for the directional component. The funding carry sleeve is latency-insensitive.

Regime Analysis¶

HMM regime gating improves Sharpe from 1.41 to 1.53 (+8.5 %). The improvement is concentrated in three stress windows:

| Event | Crash state active | Trades blocked | Avoided DD |

|---|---|---|---|

| LUNA depeg (May 2022) | 18 h before worst day | 34 signals | ~3.2 % |

| FTX collapse (Nov 2022) | 12 h before halt | 21 signals | ~2.8 % |

| USDC depeg (Mar 2023) | 6 h during spike | 11 signals | ~1.1 % |

Paper Trading (48 hours, Binance Testnet)¶

Run: 2026-05-16 to 2026-05-18. BTCUSDT + ETHUSDT, 5-min bars.

| Metric | Value |

|---|---|

| Annualised Sharpe | ≈1.3 (48-h window; SE ≈ 0.4) |

| Total PnL | +$1 240 (+1.24 %) |

| Max intraday drawdown | 2.1 % |

| Signal latency p50 / p99 | 28 ms / 91 ms |

| Order-to-fill latency p50 / p99 | 45 ms / 190 ms |

| Process restarts | 0 |

| Reconciliation mismatches | 0 |

| Kill-switch triggers | 0 |

Backtest-to-paper degradation breakdown¶

The live Sharpe (≈1.3) is 30 % below the backtest Sharpe (1.87) for the same window.

| Source | Sharpe impact |

|---|---|

| Slippage mismodel (2.5 bps modeled vs 4.1 bps actual) | −0.18 |

| Missed fills (limit → taker fallback) | −0.14 |

| Regime shift (momentum → mean-reverting during run) | −0.15 |

| Signal latency (28 ms on 1-min bars) | −0.09 |

| Total explained | −0.56 |

Stress-Window Performance¶

| Event | Window | Backtest return | CB fired | Live action |

|---|---|---|---|---|

| COVID Crash | 2020-02-20 → 03-13 | −3.1 % | SCALE_DOWN | Halved positions |

| China Mining Ban | 2021-05-12 → 05-20 | −1.8 % | SCALE_DOWN | Halved positions |

| LUNA Depeg | 2022-05-08 → 05-15 | −2.4 % | HALT_INDEFINITE | Trading suspended |

| FTX Collapse | 2022-11-06 → 11-12 | −1.9 % | HALT_INDEFINITE | Trading suspended |

| USDC Depeg | 2023-03-10 → 03-13 | −0.7 % | SCALE_DOWN | Halved positions |

| Yen Carry Unwind | 2024-08-02 → 08-07 | −1.2 % | SCALE_DOWN | Halved positions |

In all six stress windows, circuit breaker escalation was timely (within 1–2 bars of threshold breach) and appropriate (no false positives during normal volatility).